Solidifying Sustainable Corporate Value Creation Based on a Strategic Capital Policy

Toshimi Sato

Representative Director

Executive Vice President

In March 2022, the Obayashi Group formulated Medium-Term Business Plan 2022. The medium-term plan set securing a minimum of ¥100 billion in consolidated operating income and achieving a return on invested capital (ROIC) of 5% or more in the medium term as two performance targets for the period to FY2026. In FY2023, the second year of the medium-term plan, consolidated net sales exceeded the original forecast, reaching a record-high level, while consolidated operating income came in at the targets. The environment facing the Japanese economy has changed dramatically since the current medium-term plan was compiled. We have seen raw materials and energy prices soar due to the Russia-Ukraine situation as well as the rapid depreciation of the Japanese yen, disruption in global supply chains in the face of heightened geopolitical risks, and a slowdown in the global economy due to global monetary tightening. The unprecedented rise in construction material prices had a particularly significant impact, especially on projects in our domestic construction business for which we obtained priority negotiating rights prior to and including FY2021. This was one of the reasons why consolidated operating income came in significantly below the ¥100 billion level in FY2023.

We believe our corporate performance bottomed out in FY2023 due to ongoing efforts to address rising construction prices in the domestic construction business by such means as revising contract terms and conditions. Changes in the order environment are also spurring nascent improvements in profitability at the time of receiving orders. We do not expect consolidated operating income to reach ¥100 billion in FY2024. This is primarily due to several underlying factors. In the domestic construction business, large-scale properties for which we recorded provisions for loss on construction contracts are not contributing to profits as construction progress reaches its peak, and the profitability of construction project orders received when construction materials prices were rising rapidly is relatively low. In addition, in the civil engineering business, improvement in profits due to reasons including design changes for ongoing projects cannot be expected at this point. Instead, we predict earnings will steadily recover toward the second half of the medium-term plan.

Domestic construction demand is expected to remain firm for the time being. We expect construction demand to increase in multiple manufacturing fields, including semiconductors, storage batteries, machine tools, general machinery, and electrical machinery as production bases are brought back to Japan and the government designates more commodities as specified critical products. We also expect capital expenditure for electric vehicle (EV)-related facilities and for data centers to rise as decarbonization and digitalization efforts expand. In non-manufacturing sectors, we expect to see continued demand for large-scale urban redevelopment projects and the building of logistics facilities. In the civil engineering field, we foresee continued long-term demand for expressways and other infrastructure development, including renewal, and we expect construction demand to increase as the government strives to build national resilience and promote renewable energy policies.

In our overseas business, uncertainty persists in construction investment in the office, housing, and other non-manufacturing sectors in North America due to the impact of monetary policies. By contrast, construction demand is expected to remain steady in Asia as inflationary pressures ease without economies suffering significant slowdown.

We intend to take advantage of these changes in the business environment to thoroughly implement a strategy for orders that emphasizes profitability and to improve productivity. We will also strive to further improve earnings through opportune growth investments.

In the medium-term plan, we set FY2022 and FY2023 as the period for implementing measures for strengthening the foundation of the construction business and ensuring stable earnings with a consolidated operating income of ¥100.0 billion as the bottom line, while establishing a path to medium- to long-term growth with measures for accelerating transformation through FY2026.

However, due to events that went beyond anticipated changes in the business environment such as soaring construction material prices, continued growth in construction demand to levels exceeding production capacity enhancement, and changes in monetary policies overseas, profitability has been underperforming the initial plan. Moreover, in terms of safety and quality, which are essential for the survival of our business, we have been unable to eradicate serious accidents. Given this current situation, we believe that it is necessary to continue implementing thorough measures to strengthen the foundation of the construction business.

With regard to measures for accelerating transformation, we have taken this opportunity to redefine the direction of the Obayashi Group’s sustainable growth strategy by positioning the domestic construction business as our core operation and encouraging other businesses to generate performance that equals or exceeds that of the domestic construction business. In order to establish a Group business structure that can achieve this goal, we must further accelerate our efforts to build a solid management platform and pursue opportune growth investments. Meanwhile, following the revision of our capital policy announced in March 2024, and the revision of the investment plans and cash allocations for accelerating Company-wide transformation, we judged it appropriate to partially revise the performance indicator targets in the medium-term plan and issued an addendum accordingly.

Considering the Group’s current situation, in which serious accidents have not been eradicated, we will reaffirm securing safety and quality as a top management priority. This commitment will be instilled not only within the Group, but across all the people involved in the construction business including the supply chain.

Having defined the direction of Obayashi Group sustainable growth strategy, in which we are positioning the domestic construction business as our core operation and encouraging other businesses to generate performance that equals or exceeds that of the domestic construction business, our current aim is to build a Group business structure to help underpin this strategy. We also aim to grow profits through the pursuit of opportune growth investments and increased investment in human capital.

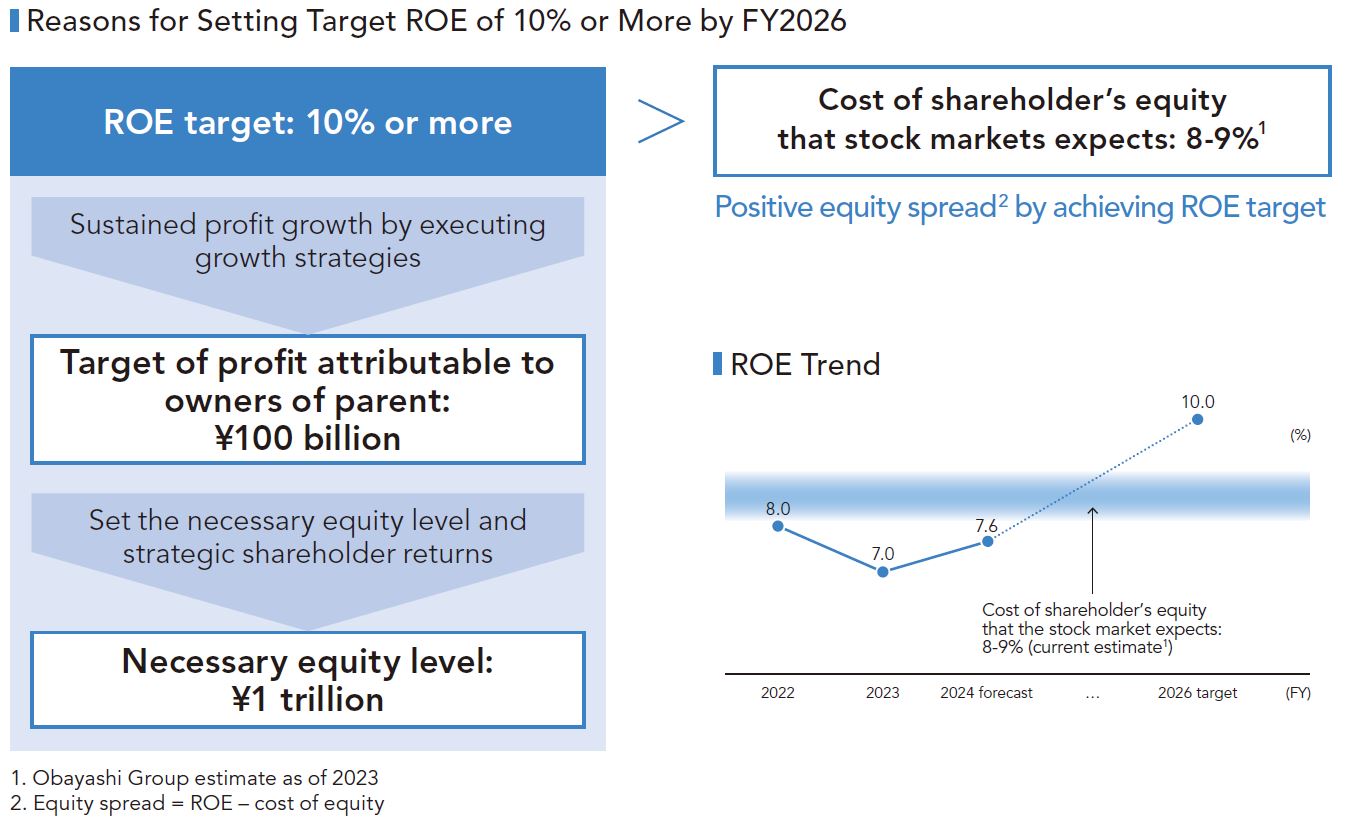

On March 4, 2024, we announced the Notice Concerning Revision of Capital Policy. In addition to setting targets for necessary equity of around ¥1 trillion, return on equity (ROE) of 10% or more, and a dividend on equity ratio (DOE) of around 5%, we also increased our targets for consolidated net sales and earnings per share (EPS) and set a new target for profit attributable to owners of parent of around ¥100 billion. Regarding investment plans for the five-year period covered by the medium-term plan, in addition to the investment allocation for strengthening our business foundation, we have increased the amount of growth investment to be used for M&A and other means of expanding our business portfolio after considering our actual performance and plans, and have revised our cash allocations accordingly.

Our ultimate goal is to position the domestic construction business as our core operation and encourage other businesses to generate performance that equals or exceeds that of the domestic construction business in order to achieve sustainable growth for the Group. With that goal in mind, we will increase total investment over the five-year period of the medium-term plan by \150.0 billion from ¥600.0 billion to ¥750.0 billion. We will also increase growth investments toward expanding our business portfolio, while striving to strengthen our management and construction business platforms. To date, ¥336.0 billion has been invested through FY2023 as follows.

Human resource-related investment is made based on the Obayashi Group Human Resource Management Policy formulated in December 2022, and we are focusing on investment in developing and securing human resources that fulfill our requirements for personnel to drive our core domestic construction business and personnel required to achieve our growth strategies. Regarding investment in DX initiatives, technology, construction machinery and business facilities, and other relevant areas, we have been implementing investments designed to improve productivity ahead of the application of regulations to cap overtime work in the revised Labor Standards Act of Japan from FY2024.

In the real estate development business, we are looking to diversify asset types by expanding the scope of our business from offices to logistics and other facilities, and to globalize our business portfolio by developing and acquiring properties in London and developing properties in Thailand. We are also using the private fund established by the Group to refresh our asset portfolio and improve our investment efficiency and profitability.

Regarding M&A opportunities, MWH US Acquisitions, Inc., a major constructor of water treatment facilities in the United States, became a subsidiary. Our aim is to expand our business in the U.S. water-related infrastructure construction area, which is expected to enjoy stable growth. We also intend to promote further MWH growth by providing the company with the opportunity to utilize our technologies and resources, by providing financial support, and through collaborative measures with existing Group companies in the U.S. Meanwhile, we have acquired a 50% stake in Eastland Generation Limited, a renewable power generation company in New Zealand, and made it an affiliate. Going forward, we will be looking to apply the expertise and leverage the networks that the Group has cultivated in Japan and New Zealand to create synergies that can help promote further growth for Eastland Generation’s renewable power generation business.

The medium-term plan stipulates that the Group works to strengthen the business foundation and accelerate Company-wide transformation, and targets a minimum return on invested capital (ROIC) of 5% or more over the medium term as one of the performance indicators for promoting management that emphasizes capital efficiency.

In order to meet this target, we will secure sustainable profit growth for each of our businesses while controlling invested capital. Upon considering the need for a capital structure that focuses more strongly on capital efficiency, including the use of leveraged financing, we have set the level of necessary equity at ¥1 trillion. We aim to achieve ROIC of 5% or more in the medium term and ROE of 10% by FY2026, the final year of the medium-term plan. We intend to achieve this by promoting measures for 1) sustainable profit growth by executing a growth strategy and 2) setting a necessary equity amount and strategic shareholder returns.

We generate sustainable profits by further enhancing investment in human resources, DX, technologies, and productivity improvement to continue to fulfill the social mission of the construction industry while giving top priority to safety and quality against the background of the decline in the number of engineers and workers in the construction market.

We identify fields where the Group can establish a competitive advantage in contributing to the solution of social issues, such as carbon neutrality and well-being or fields with potential for growth for each business. We will increase profits by implementing proactive and timely growth investment in the identified fields.

In order to optimize Obayashi Group growth centered on the construction business, we set invested capital to reflect the capital cost requirements for each business and determine the necessary equity amount based on the capital structures of each business (including the use of leveraged financing). The necessary levels of invested capital and equity capital are reviewed as needed depending on the scale of business operations and other factors. The Board of Directors will evaluate the capital structure and balance sheet of each business according to the potential impact on the Group’s capital efficiency.

We set the necessary equity of the Group during the period covered by the medium-term plan at the one trillion-yen level and will execute strategic shareholder returns. With regard to shareholder returns, we have raised the dividend threshold set forth in the medium-term plan from a dividend on equity ratio (DOE) of around 3% to DOE of around 5%, giving top priority to offering stable dividends over the long term. We will offer returns even more flexibly through special dividends, share buybacks, and other methods by making comprehensive judgements based on these parameters and after taking into account the amount of necessary equity, level of profits, financial position, price-to-book ratio (PBR), and other factors.

Obayashi Corporation holds shares in customers’ businesses (cross-shareholdings) for the purpose of maintaining and strengthening business relationships. We have constantly been verifying the medium- to long-term economic rationale of these cross-shareholdings and we sell holdings whose significance has diminished from a business perspective based on a comprehensive consideration of capital costs, business returns, and other profitability-related factors and valuation risks. We use the cash generated from the sale of cross-shareholdings to increase corporate value, effectively investing in vehicles that offer stable income and in new areas that contribute to sustainable growth.

We are further reviewing the significance and efficiency of cross-shareholding investments as part of the medium-term plan. We started selling those holdings in FY2021 with the aim of reducing cross-shareholdings to 20% or less of consolidated net assets as soon as possible before the end of March 2027. We sold a total of ¥74.6 billion in cross-shareholdings over the three years from FY2021 through FY2023 (consolidated and market value basis). That total increases to ¥146.3 billion when combined with sales that have been agreed on but not yet executed. Having said that, due to the rise in the share prices of those holdings, the balance of cross-shareholdings rose to ¥403.5 billion at March 31, 2024, on a market value basis, accounting for 33.8% of consolidated net assets.

We will not be swayed by trends in the stock market, but will further accelerate the sale of cross-shareholdings by setting the balance of cross-shareholdings to 20% or less of consolidated net assets as a mandatory target.

To increase Obayashi Group corporate value while also striving to secure steady growth, we have to achieve a level of ROE that exceeds the cost of shareholder’s equity expected by stock markets

(currently assumed to be 8% to 9%). We are aware that a positive equity spread is what enables achievement of investment-driven extended reproduction, a recurrent or cyclic process.

The Obayashi Group intends to build a bridgehead for its growth strategy not only by improving productivity through DX-related and technology-related investments, but also by steadily pursuing growth investments that capitalize on potential opportunities and increase competitive advantage, strategic investments in human capital, and other investments. We will also solidify our sustainable corporate value creation by pursuing a strategic capital policy that focuses on capital efficiency, and steadily enhance Obayashi Corporation’s corporate value and shareholder value.

September 2024